What is home equity

Home equity is one of the most important benefits of being a homeowner. So, what is it exactly?

Simply stated, home equity is the ownership stake you have in your home — the difference between your home’s current value and your current mortgage balance (or balances if you have a “second mortgage” like a home equity loan).

How do you use home equity?

You can access a portion of your home’s equity and turn it into cash (keep reading to find out how). And you can use this cash however you like:

- Consolidate high-interest debt, like credit cards *

- Make home repairs and improvements

- Cover an unexpected expense or emergency

- Pay off student loans and more

Keep in mind, if you use your home equity for home repairs and improvements, the interest you pay may be tax deductible. (Check with a tax advisor for details.)

* “Paying off unsecured debt with a HELOC makes it secured.”

How do you build home equity?

Your home equity generally grows two ways:

- As your home gains value. This could be from market improvements or through home improvements.

- You can accelerate this growth by paying additional principal and interest each month or by using a bi weekly payment plan.

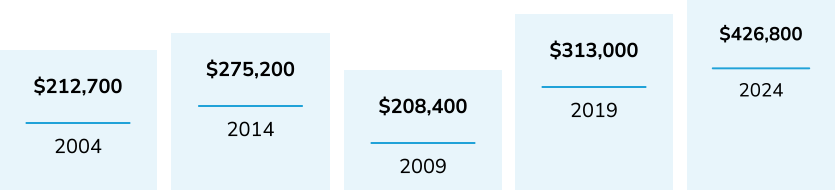

Did you know: Your home equity grows as your home’s value grows.

Home values in the U.S. have soared over the past two decades:

Source: fred.stlouisfed.org

Making a larger down payment when you buy your home is another way to build home equity faster.

How do you calculate your home equity?

Home equity is calculated by subtracting your mortgage balance (along with any second mortgages like a home equity loan or HELOC) from your home’s current value.

So, if your home’s value is $500,000 and your mortgage balance is $300,000, you “own” $200,000 of your home. This is your total home equity. With a HELOC, you can access up to 80% of your home equity. In this example, your available home equity would be $160,000.

Let’s take a look at the math:

How can you access your home equity?

There are a few ways to turn your home equity into cash for home improvements, debt consolidation, or whatever you need. Here are two of the most common:

- Home Equity Line of Credit (HELOC) — a line of credit that lets you access the cash you need without refinancing.

- Cash-Out Refinance — a more involved process in which you refinance your current mortgage for more than you owe and take the extra loan amount as cash.

No matter which option you choose, keep in mind that accessing your home equity can be a smart way to get the funds you need for pretty much anything.

Learn more about a Homebridge HELOC!

Check your rate and choose your amount risk-free!